Innovative financing mechanisms to bridge the digital divide

| Attachment | Size |

|---|---|

| English | 2.59 MB |

Organization

Innovative financing mechanisms to bridge the digital divide

Since the start of the World Summit on the Information Society (WSIS) process, after more than 20 years of deployments in developing countries, traditional telecommunication and mobile network operators have yet to meet universal access goals, even for basic voice connectivity.[2] The continued inability to meet universal service aspirations amply demonstrates that ensuring the WSIS vision of “a people-centred, inclusive and development-oriented Information Society, where everyone can create, access, utilize and share information”[3] cannot be left solely to traditional telecommunication incumbents to solve.

Within this context, it should be noted that the pursuit to bridge the digital divide in underserved or remote areas pre-dates WSIS. It has been a longstanding challenge, first identified in The Missing Link, also known as the Maitland Report,[4] published in 1985 by the International Telecommunication Union (ITU), and since then in many ITU development forums and global information society discussions. The shift in focus from access to telephony, to broadband internet, and now to meaningful connectivity[5] underscores the changing landscape of digital inclusion. However, the absence of a business case that meets the profitability requirements of traditional commercial operators continues to pose significant challenges for these players to offer services that can bridge the digital divide in remote and rural areas with small populations.

Given that traditional strategies are failing to close digital gaps in the global South, multitudes of national and international workshops and discussions have taken place that have now begun to consider the role of innovation in financing mechanisms for addressing the digital divide. Within this context, the critical role of new and innovative financing mechanisms is now more widely accepted, and community-centred connectivity solutions are gaining increasing attention as strategies to close the digital gaps.

Background on financial mechanisms as part of WSIS

During the first phase of the WSIS process, one of the issues on which consensus could not be reached was the creation of a Digital Solidarity Fund (DSF), which was supported by many developing countries, but was resisted by many donor countries, who preferred to adhere to the agreements of the Monterrey Consensus. As a result, to study the proposal of a DSF ahead of the second phase, a Task Force on Financial Mechanisms (TFFM) was established by the UN Secretary-General. It was chaired by United Nations Development Programme (UNDP), and included APC among its members. Although initially concerned with the proposal to establish a UN-led DSF, the TFFM remit ended up being extended to review the adequacy of existing financial mechanisms, and to propose “improvements and innovations of financing mechanisms” including the DSF.[6] The DSF was inaugurated in 2005, before the Tunis meeting and without waiting for the TFFM’s blessing, and its funding was dependent on an innovative financing mechanism known as the “1% digital solidarity contribution”, which was a voluntary commitment of local and national governments and the private sector who agreed to introduce the 1% digital solidarity clause on all their bids relating to information and communications technology (ICT) equipment and services. This meant that the vendor who won the bid contributed 1% of the transaction price to the DSF.

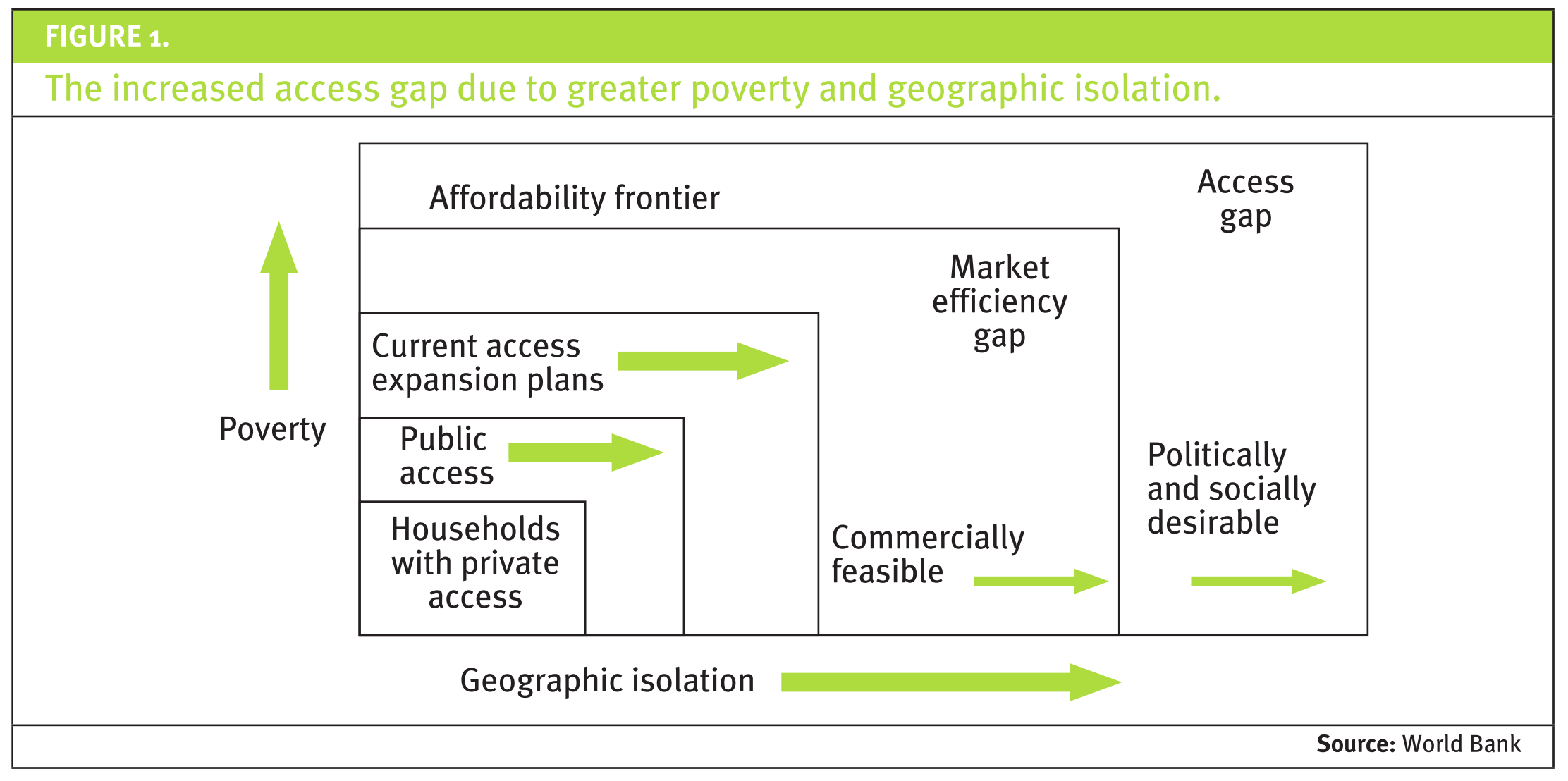

The most important conclusion from the TFFM was to highlight the vital role of public finance in closing the digital divide. This is important because donors and the international financial institutions had effectively been withdrawing from this area since the early 1990s as private capital stepped in. However, it was clear that private capital driving profitability for maximising shareholder value had proven to be insufficient incentive to fund the connectivity needs for bridging the digital divide, particularly at the local level and in remote regions where efforts to ensure an inclusive information society are most needed.[7] A pioneering report from the World Bank [8] visualised the underlying reasons behind this funding gap clearly (see Figure 1). The report has since influenced many discussions that called for more countries to create or use their existing universal service funds (USFs) and called for their implementing agencies to more effectively bridge the digital divide using them.

Figure 1. The increased access gap due to greater poverty and geographic isolation. Source: World Bank

USFs were first implemented when countries began to privatise and open up the telecommunications industry for greater competition. The aim was to impose a “universal service fee” based on a small proportion of the revenues of operators who had obtained licences in profitable areas. These funds were then to be used to offset the higher costs of provisioning infrastructure in rural areas, as well as providing a mechanism for attracting more providers to apply for licences for universal access.

The United States was the first to establish a USF, promulgated in its 1996 Telecommunications Act. Many other countries followed, but the adoption of USF strategies was not as widespread as expected, and the funds have often not been fully disbursed or have been inefficiently spent on under-used services. In light of this, the TFFM highlighted the potential role of unlocking USFs (if adequately resourced and managed) as a driver for the coordination of not only the funds from the telecommunications industry but also as a mechanism to attract external funds.

The TFFM's findings and conclusions were incorporated into the recommendations of the Tunis Agenda, including a) “Helping to accelerate the development of domestic financial instruments, including by supporting [...] networking initiatives based on local communities” and b) “Strengthening capacities to enhance the potential of securitized funds and utilizing them effectively.”[9]

Evolution of financial mechanisms after WSIS

As an indication of the extent of funding required to achieve universal access to broadband by 2030 at the global level, the ITU estimated in 2020[10] that the total capital required would be about USD 428 billion. Its study proposed to split the funds needed between public (25%) and private finance (75%), drawing mostly on private investments for infrastructure, and public investments for skills and policy.

The DSF closed in 2009 after being said to have only raised USD 6.4 million. The Digital Development Partnership (DDP) created in 2017 and coordinated by the World Bank could be considered as helping to fill the gap in funding left by the DSF, even if only around knowledge production, technical assistance and unlocking finance. The DDP has raised USD 50 million from different donors since its inception, mainly in development aid from global North governments. Its work has also led to leveraging over USD 10 billion in lending and investment operations,[11] primarily through its Digital Development Global Practice programme.[12]

More recently, the pledge platform of the Partner2Connect multistakeholder initiative launched by the ITU and the Office of the UN Secretary-General's Envoy on Technology[13] has become a central space for expressing economic commitments to closing the digital divide. However, it lacks mechanisms to ensure that those commitments are effectively met. Another innovative financial mechanism that is yet to show significant results is Giga, the UNICEF/ITU initiative that aims to mobilise USD 5 billion to provide connectivity in schools.[14]

Concerning public finance from multilateral development banks (MDBs), investment in the ICT sector has in general been relatively limited. A study by the Alliance for Affordable Internet (A4AI) showed that “only around 1% of MDB cumulative commitments to projects in low- and middle-income countries over the 2012-16 period were specifically targeted towards the ICT sector, or had ICT as a primary project component.”[15] This means that only about USD 5 billion in cumulative funds were invested in the entire sector in the period. Among other things, the A4AI study stressed the need to “change the investment narrative within and outside of MDBs to re-establish the ICT sector as a priority sector.”

This narrative seems to be indeed changing, with initiatives such as the World Bank committing USD 25 billion to connect all African governments, businesses and citizens to high-speed broadband by 2030, or by the inclusion of “Enabling Digitalization” as one of eight priority areas of their new vision of “a world free of poverty on a livable planet”.[16] Other initiatives looking at financing telecommunications infrastructure in rural areas include the recent European Commission’s Global Gateway,[17] which aims at unlocking EUR 300 billion for five key areas, one being digital infrastructure, and the G7-led Partnership for Global Infrastructure Investment, which aims to mobilise USD 600 billion in energy, physical, digital, health and climate-resilient infrastructure in low- and middle-income countries by 2027.[18] Both initiatives are rooted in countering the influence of China, which, through the Digital Silk Road component of its ambitious Belt and Road Initiative, was estimated to have already invested USD 79 billion in projects outside China by 2018.[19] However, these investments are primarily aimed at supporting the same traditional actors to consolidate their existing infrastructure and invest in advanced services such as 5G in urban areas.

Nevertheless, all these financing commitments combined still fall far short of the ITU’s USD 428 billion estimate of the needed funds. The UN Conference on Trade and Development’s World Investment Report 2023 similarly concluded that the increased level of investment required is not taking place, stating that “the contribution of international investment to SDG [Sustainable Development Goal] 9.c (access to information and communication technology, and universal and affordable Internet coverage) remains limited.”[20]

At the national level, although progress has been made in the number of countries establishing USFs, growth has been less than expected (only about 42% of ITU’s member states reported a fund in 2021).[21] In addition, the functioning of USFs is not meeting expectations in most countries, as indicated in the 2022 report on Financing for Sustainable Development from the UN Inter-Agency Task Force on Financing for Development.[22] The report’s main recommendation proposes to look at how “[u]pdated universal service and access funds (USAFs) could help to pool funds and provide expertise to achieve universal and inclusive broadband coverage and use.” The report acknowledges the difficulties of managing USFs reported elsewhere,[23] and considers even the possibility of discontinuing them in countries where fixing them is too difficult. Reforming USFs as a mechanism is also proposed by the Broadband Commission in its report on 21st Century Financing Models for Bridging Broadband Connectivity Gaps,[24] as well as by the DDP, which currently has a project in its portfolio titled “Reaching the bottom 10%: Financing, policy and regulatory models and country case studies” that looks at providing recommendations for a new model for USFs.

The Financial Mechanisms section of the WSIS+10 review resolution also supports a prominent profile for ICTs in the Technology Facilitation Mechanism (TFM) established in the Addis Ababa Action Agenda of the Third International Conference on Financing for Development.[25] However, the outputs of the TFM do not indicate any specific solutions that may have contributed to bridging the digital divide.[26]

In contrast to the public finance efforts, a clear trend in the last 20 years has been the massive influx of private capital into the telecommunications industry, and the adoption of innovative technologies requiring lower capital costs in mobile, satellite and fibre, both terrestrial and submarine, along with the explosion of Wi-Fi in the last mile, which has been dramatic. This, and the push to deregulate and privatise the telecommunications industry, have created many opportunities for private capital to profit from these new innovations. With the proliferation of capital-intensive, privately owned low earth orbit (LEO) satellite companies, along with the extension of 5G networks by mobile operators, there are opportunities to address universal access; however, the private capital used to fund these new technologies tends to focus on the more profitable markets that maximise the returns for their shareholders. Furthermore, despite subsidies from USFs, operators find the return on investment insufficient to justify the cost of offering services and maintaining their infrastructure in less profitable areas, perpetuating the challenge of bridging the digital divide.

Even where sufficient numbers of users exist to justify the infrastructure investment, statistics from GSMA, the association representing mobile operators globally, show that in rural areas, traditional operators are only able to provide traffic-capped mobile data services, which are unaffordable for the general population in those areas.[27] Hence, the absence of a clear business case for offering affordable, uncapped high-speed services in areas with low average revenue per user (ARPU) continues to pose a significant hurdle.

This reality of the high cost of value-added services highlights the need to transition from financing mechanisms based on models that meet universal coverage targets included in the SDGs, to those that meet the meaningful connectivity targets established by the Office of the UN Secretary-General’s Envoy on Technology, and the ITU.[28] Despite some unlocking of new funding sources and improvements in USFs, challenges in financing infrastructure for bridging digital divides still persist 10 years after the last WSIS review. As long as we rely on traditional players and private investment approaches that prioritise profitability, these divides will continue to widen. Public funds channelled through traditional USF models also seem insufficient, and the mechanisms created as part of the WSIS follow-up process do not appear to have had a significant impact. Clearly we need additional sources of finance from non-traditional funders using innovative and flexible financial mechanisms along with a regulatory environment that allows many more complementary network operators to emerge that are socially focused on bridging the digital divide as opposed to solely focused on profitability. Ultimately, to improve the balance between profit maximisation and the goal of reaching universal access, the time has come to fully review where socially driven investments are made and how effective they are at addressing digital inclusion.

Including more cost-effective complementary network providers in the financing mix

ITU Secretary-General Doreen Bogdan-Martin has stressed that to achieve meaningful universal connectivity, “business as usual” will not work.[29] Reinforcing this view, the business case for the deployment of digital infrastructure in most unserved and underserved populations appears more favourable to decentralised, local or community-centred connectivity providers. This has led to the emergence of community networks and social enterprises as alternative or complementary network providers in many regions. These providers are driven by completely different investment imperatives, bringing unique assets to the economic calculus of deployment.[30] They are part of the ecosystem of micro, small and medium-sized businesses that are the lifeblood of so many economies around the world, especially in the developing world, but that have been neglected for a long time in the telecommunications sector used to building large networks.

In remote, sparsely populated areas, connectivity provision by traditional operators is not a priority given the small scale of potential revenues and the much higher costs of backhaul, energy, transport and sourcing of the business and technical skills, which are usually scarce in these areas. This contrasts with the business case of local, community-centred connectivity providers that can start at a very small scale and have a more diverse range of ownership and operating models for achieving financial sustainability for their operations.

To address startup costs, many community-centred operators fundraise internally, especially if there are some businesses or other organisational users willing to commit to being anchor tenants (ideally with an upfront payment for services). However, in most rural areas in the developing world, the resident population is unlikely to have the financial capacity to provide all of the needed resources, so in most cases some form of external funding is required. Grants and awards from charities and civil society organisations, the support of the technical community, as well as corporate social responsibility (CSR) schemes donating equipment and premises to host equipment or towers, have all contributed to lowering the outstanding capital expenditure necessary to set up a network.[31] Although largely untapped, there are also cases of national, state and local public administrations financing initial deployments.[32] Overall, however, while operational and maintenance costs can be sustained despite low ARPU, initial startup costs will still require raising external funding, and this is where some innovative funding mechanisms and funding sources can be explored.

To address operational and maintenance costs, while some community-centred connectivity providers operate similarly to traditional commercial networks where user fees cover all the setup and operating costs, others often reduce costs by drawing on the local community for volunteer labour, donations of upstream bandwidth, and the permission to use high sites to erect towers. They are sometimes able to tap into subsidies from government and other commercial sources. Some also innovatively obtain funds by offering services such as e-payments, energy provision/charging, and hosting local information servers or remote sensing equipment (weather, air quality, etc.) for a government programme or research agency.

The key point is that by being community-centred (structured as NGOs, social enterprises or community-owned networks) as opposed to profit-centred, most community-centred connectivity providers are not constrained by the need to provide the kind of return on investment that commercial investors require. They also do not need to spend money on costly marketing or public relations, as there is typically a high level of awareness among community members about the network. As a result, substantially higher sign-up rates for community-centred internet service providers (ISPs) as opposed to incumbents are often observed, which substantially (and favourably) changes the economics. This leads to a markedly lower cost of customer acquisition, again favourably improving the economics for community-centred providers.

In addition, with only a modest amount of training required, community-centred service providers can also build the capacity of community members to contribute, especially women. These trained community members are able to take responsibility for most tasks required by the operations, such as erecting towers and installing equipment on roofs, or even day-to-day technical and administrative tasks (troubleshooting, adding users, collecting fees, etc.), thereby significantly reducing their overall operating costs. Many of these providers have also used innovations in energy-efficient equipment powered by green energy, lowering their operating costs significantly. Last but not least, they are able to use a cross-subsidisation model, where local businesses pay a monthly fee that allows discounts for end users.

Beyond being more cost effective, these community-centred models allow broader participation of diverse community members to address their needs, which tend to go beyond the provision of connectivity on its own. For example, this includes building digital skills and creating local digital content that is culturally sensitive and relevant. Because of this, the case for community-centred connectivity providers has the added advantage of bringing many important social and economic benefits to the community, as described elsewhere.[33] It may be difficult to translate some of these benefits into the return on investment needed to pay for the network and its operations, but the benefits clearly make a strong case for funding these solutions for more effective digital inclusion.

While there have been some examples of innovative financing mechanisms to support community-centred connectivity providers, the financial resources currently available are insufficient to help them scale up. Attempts to engage commercial financial institutions that invest in traditional communications infrastructure to increase the options for financing community-centred operators have surfaced three difficulties that need to be addressed: their limited scale, their high real and perceived levels of risk, and their lower returns on investment.

However, we believe that with sufficient will from different financial stakeholders to address these difficulties (including understanding the benefits of community-centred networks beyond strict return on investment calculations), focusing on funding community-centred service providers is a more cost-effective way to bridge the digital divide effectively, compared to trying to incentivise and fund large private telecommunications companies to do so.[34]

As mentioned above, while some community-centred connectivity providers are steadily building solutions to persistent digital divides, their relatively small size and limited number underscore the struggle to access capital to expand or seed new networks. To address these funding constraints, there is a strong need to create an enabling and flexible policy, regulatory and financing environment that encourages the emergence of more innovative local and regional investment models for community-centred connectivity providers, which allows them to expand and operate cost-effectively.[35]

Leveraging increased recognition of community-centred connectivity providers

Community networks were recognised in 2019 in the UN Economic and Social Council (ECOSOC) resolution on the “Assessment of the progress made in the implementation of and follow-up to the outcomes of the World Summit on the Information Society”.[36] At the ITU level, the recognition of “complementary networks” as a solution to bridging the digital divide at different national and regional levels was crystallised at the World Telecommunication Development Conference in 2022 (WTDC-22) in Resolution 37 (Rev. Kigali, 2022), which resolves to instruct the Director of the Telecommunication Development Bureau (BDT) to “continue supporting Member States, where requested, in developing policy and regulatory frameworks that could expand and support the engagement of telecommunication/ICT complementary access networks and solutions in bridging the digital divide.”[37] The 2024-2027 Kigali Action Plan resulting from the WTDC also includes community networks in the expected results for two of the priorities for the Americas region for this period. Giga, meanwhile, considers community networks among the models that can contribute to delivering connectivity to all schools by 2030.[38]

However, greater recognition of the role of community networks is not enough. Key policy and regulatory elements also need to be in place for this initial recognition to translate into access to capital and ease of operation for these providers. Primarily, there needs to be an appropriate licensing framework for small social-purpose operators that incentivises them to contribute to solving the challenge. Among those incentives, lowering licence fees, or even waiving them, and reducing their administrative burden, are among the most important. At the national level, a few countries around the world are leading the way and have already created community network categories in their licensing frameworks. In Africa, Zimbabwe,[39] Uganda,[40] Ethiopia[41] and Kenya[42] have all included community networks within their regulatory frameworks, while South Africa proposes to include a new licence category specifically for community networks[43] following the recommendations from the Competition Commission that deemed mobile network practices anti-poor and requested support for alternatives.[44] In Latin America, similarly, Mexico and Argentina have created provisions for their recognition, with Colombia[45] and Brazil[46] working actively to enable them within their current frameworks.

This aligns closely with the recommendations in the Best Practice Guidelines from the ITU’s Global Symposium for Regulators held in 2021, which specifically state that “[r]egulatory tools are at hand to bridge the funding and financing gap in digital markets” and identify the need to “[p]romote local innovation ecosystems and provide incentives for the participation of small and community operators in deploying low-cost rural networks, including specific licensing measures, access to key infrastructure and funding, and social coverage promotion programs.”[47]

The guidelines, together with recommendations from the Broadband Commission, among others, also point to another related enabler: the need of community networks to access the mobile spectrum that is usually either unused or unassigned in rural areas in the global South. Mobile spectrum offers opportunities to bridge the digital divide more cost-effectively, including meeting Target 9c within the SDGs. Approaches to spectrum sharing are becoming widespread in the global North, but their adoption in the global South, where they are most needed, is still the exception.

As indicated earlier, a key source of funding would be from USFs, an important enabler that some governments are now starting to operationalise. Here progress has been slower, but change is starting to accelerate, especially in countries where a community network licence exists. The interest from regulators and policy makers is generally on the rise, as indicated by various workshops organised by APC in collaboration with ITU-D, the ITU’s development sector, after Resolution 37 was approved – in Kenya, Indonesia, Nigeria, Cameroon and Colombia – and with regional regulatory agencies such as CRASA in Southern Africa and CITEL in the Americas. In addition, recent reports from the Broadband Commission[48] recommend that community networks should be beneficiaries of USFs for extending affordable broadband access to commercially challenging rural and remote areas, to women and to low-income users.

In an example of USF funding specifically for community networks, Argentina created a mechanism within its USF to both incentivise the adoption of a community network licence and the use of the fund to help establish connectivity providers in underserved communities.[49] This mechanism does not prevent the regulator from supporting more traditional approaches, since the USD 3 million dedicated to these programmes represented 0.63% of the regulator Enacom’s 2020-2022 budget.[50]

Similarly, in Kenya, its USF Strategy 2022-2026 is now looking to adopt financing mechanisms that will support 100 community networks and other complementary connectivity providers.[51] In both countries, civil society is playing an important role in building the capacity of these providers to meet regulatory requirements and to encourage collaboration between disparate projects. In addition, other countries such as Malawi[52] and Papua New Guinea[53] have proposed supporting community networks in their USF strategic plans for the coming years. This trend is expected to continue following the ITU’s inclusion of community networks as one of the innovations recommended in its USF toolkit.[54]

Beyond support from USFs, the Broadband Commission report on financing models proposes that community networks should be beneficiaries of other types of support from public sources, at the national and international level.[55] In recent years, international financial institutions such as the World Bank, the Inter-American Development Bank[56] and the Asian Development Bank,[57] and other regional financial initiatives such as the European Commission's Global Gateway, have now also begun to show interest in these types of small local providers.[58] However, financial solutions from these institutions have yet to materialise, partly due to the relatively recent emergence of community connectivity providers.

From recognition to tangible action

Although the Tunis Agenda already included the importance of “supporting [...] networking initiatives based on local communities,” the reality is that over the last 20 years, community-centred connectivity initiatives have evolved, for the most part, in relatively challenging environments. The majority of regulators in the sector have not expanded their views outside of the narrative that views private companies as the only model for providing telecommunication services. Hence, licensing frameworks and financial mechanisms are designed to privilege private sector participation in the industry. While this has had many positive effects, closing the digital divide is not among them. On the contrary, as the COVID-19 pandemic showed,[59] the divide is intensifying.[60]

We believe that now is the time that those participating in the WSIS process recognise that community-centred models are not receiving enough attention, and there needs to be more proactive engagement in supporting these complementary solutions that are critical to ensuring the inclusion of marginalised groups such as women and Indigenous communities, as well as the most financially disadvantaged. In particular, to unlock financial mechanisms for digital inclusion and solidarity, it is crucial to ensure community-centred approaches to digital inclusion are featured more prominently in events where financing for development will be discussed. This includes processes such as the Global Digital Compact (GDC), where the role of community-centred approaches requires more explicit attention in order to counterbalance the prominent role in the debate of multinational companies, whose profit-maximising needs are in conflict with the needs of those excluded from the information society.

There are positive signs that certain governments, UN agencies and multilateral actors, including financial institutions, are starting to recognise the role that community-centred initiatives can play. We welcome this trend. At the national level, some governments are creating space for these initiatives within their telecommunications licensing regimes, and in some specific cases, allowing them to access mobile broadband spectrum. But those countries remain, by far, in the minority.

In order to be successful, any financing mechanisms must be part of a larger enabling environment for community-centred operators. But the centrality played by private companies in the telecommunications sector, and their success in expanding services to the market frontier, has distracted from the need to also create an enabling environment for other alternatives. Because of this, it is critical that digital exclusion is considered by all WSIS actors as a development problem that transcends the dynamics of the telecommunications industry. Despite the positive trend in recognition that community-centred approaches have achieved, much needs to be done to raise awareness of community-driven alternatives to bridging the digital divide and how to create innovative, affordable and flexible financial products that enable them to sustain their businesses.

Some steps have been taken to bridge this gap,[61] but much more is required.

Unlocking financing mechanisms for community-centred connectivity providers to complement existing solutions to close the digital divide is a frontier area of work, which could be compared to the early days of microfinance for underserved communities and businesses. The challenge today is to mainstream, accelerate and incentivise more innovative financing and investment models for new community-centred operators, and for expansion and upgrades for existing operators, while providing the enabling regulatory environment and training needed at each stage of development for their long-term sustainability.

Action steps

Based on the above discussion, the following key recommendations can be made to inform the WSIS+20 process going forward:

- Commission on Science and Technology for Development (CSTD) should convene a series of workshops to help multilateral development banks and other public finance institutions better understand community-centred network providers and explore financial mechanisms within their mandate to support community-centred connectivity solutions.

A potentially important venue for this could be as part of the preparations for the Fourth International Conference on Financing for Development scheduled to take place in Spain in 2025.[62] This includes the Summit for the Future, where linkages between the GDC and reforms to the international financial architecture should be established as part of the long-term financing of sustainable development.[63] The workshops should result in a clear action plan that goes beyond high-level recommendations to include a minimum testing of some of the solutions already suggested in the reports from the TFFM, Giga and the Broadband Commission, with a particular focus on countries where the regulatory environment is already conducive to these approaches.

- In parallel, policies and regulations need to be adapted to provide a more supportive enabling environment for community-centred connectivity providers.

This includes streamlining licensing processes and reducing licence fees, making spectrum available and minimising reporting burdens.

- Incentivise more local and regional socially driven impact funds that financially support new complementary network providers focused on digital inclusion.

Innovative funding mechanisms include blended finance catering to the scale and perceived risk level of community-centred solutions. These innovative instruments are run by socially driven funds which assess risk and impact differently from the traditional project viability or credibility assessment schemes that institutional funders are acquainted with. New specialised funds which invest in small-scale infrastructure are already emerging and successfully supporting community-centred solutions. Examples include Connectivity Capital and Connect Humanity. They have leaner structures and understand the local context better, resulting in lower transaction costs than more traditional funds in the telecommunications industry. This means these new initiatives can support a variety of small-scale and community-centred approaches, showing that making these types of investments is a viable strategy. Many other regional, national or local social impact funds, such as FISIQ and Angels of Impact, could be encouraged to follow these examples and invest in community-centred connectivity providers. An additional advantage of these impact actors is that they can disburse and manage funds in amounts that can be effectively absorbed by community-centred providers, something that is much more difficult for the instruments of development finance institutions and other large investors, which are designed to manage multi-million dollar disbursements. It is important to note that these specialised intermediaries are already pervasive in many other sectors of development finance and financial assistance and there is an opportunity to incentivise them to add digital inclusion to their portfolio with support from public finance.

National governments can in turn support these funds via tax incentives as well as through direct investment from USFs or other government mechanisms as well as using tools such as guarantee pools, first-loss investments and other credit guarantees. This will allow new social investors to expand the range of their integrated capital mechanisms to be more effectively applied here.

- Review current financing mechanisms and strengthen existing funding interventions.

Given the multiple voices requesting revision of USF models to encompass support for community-centred approaches, the recommendation to act on this swiftly is an obvious one. USF funds should flow either directly to community-centred network providers or through new or existing social impact investors, thereby creating more effective incentives to channel investment for public-private partnerships, tax breaks for donations, and the modification of public procurement guidelines. Community networks can also participate, and conditional funding from multilateral development banks can also be used to create enabling frameworks. There are already mechanisms for this such as the World Bank’s Development Policy Financing.[64] Providing guarantees so that local banks can also offer financing products to these providers would be helpful too.

In addition to the role of government and multilateral funding agencies, the potential role of philanthropy in unlocking supporting funds should not be underestimated. Although it has been observed that their role in the ICT sector is currently relatively small,[65] with only 0.05% of US philanthropic funds going to digital equity-related projects,[66] some charities are starting to take much-welcomed action[67] and could play a more central role in addressing digital exclusion. While philanthropic dollars have traditionally been used to support digital skills, funds can be used as catalytic investments in USF social impact funds to support investments into community-centred network providers.

- Ensure replication of solutions by raising awareness of community access solutions in rural communities as well as among policy makers and financiers.

For these recommendations to be successful, awareness raising is needed among the rural communities that could become community-centred connectivity solution providers. It is also critical to raise more awareness among policy makers and financiers about community-centred connectivity as the best-positioned model to end the digital divide.

- rural communities’ capacity to access financial mechanisms.

Building the human capacity, not only technical but also financial, of those who wish to take advantage of these new mechanisms is equally critical. As such, there is a need to provide technical assistance to increase the investment readiness of community-centred connectivity providers and thereby build a pipeline of investment opportunities for the financial products mentioned above. This assistance can be provided by the social impact funds mentioned above in partnership with local civil society organisations. Working with structurally marginalised communities as internet service providers differs significantly from the traditional operation of the telecommunication sector. In this context, it is encouraging to see local civil society organisations supporting community-centred connectivity providers.[68] They are more familiar with the ecosystem and can thus better evaluate potential opportunities, aggregate needs, and provide legal and administrative support, and so can be partnered with to offer the customised skills needed.

If we want to make progress in the WSIS goals for digital inclusion, we need to do something more. We should take this opportunity to reflect on what WSIS has achieved, and recognise that traditional players and traditional financing mechanisms have not solved the problem. That includes the incapacity of their business models to offer affordable, uncapped high-speed services in areas with low ARPU, which in turn prevents them from meeting the meaningful connectivity targets established by the Office of the UN Secretary-General’s Envoy on Technology, and the ITU. The problem requires innovative business and financial models that can better leverage public, private and philanthropic finance to reducing digital exclusion. We should therefore take a broader view on how best to support new, innovative, socially driven investors who can better support community-centred connectivity providers focused on bridging the digital divide.

Footnotes

[1] The authors are grateful to Steve Song, Jochai Ben-Avie and Willie Currie for their feedback on the original draft, as well as to Valeria Betancourt, Anriette Estherhuysen and Karen Banks for their pointers to relevant sources.

[2] Shanahan, M., & Bahia, K. (2023). The State of Mobile Internet Connectivity 2023. GSMA. https://www.gsma.com/r/somic/?ID=a6g1r000000xnptAAA&JobID=1709262

[4] ITU. (1985). The Missing Link: Report of the Independent Commission for World Wide Telecommunications Development. https://www.itu.int/en/history/Pages/MaitlandReport.aspx

[5] According to the UN’s Broadband Commission, “meaningful universal connectivity” encompasses broadband that is available, accessible, relevant and affordable, but also that is safe, trusted, user-empowering and leads to positive impact. See: https://www.broadbandcommission.org/universal-connectivity

[6] Souter, D. (2007). Whose Summit? Whose Information Society? Developing countries and civil society at the World Summit on the Information. APC. https://www.apc.org/en/pubs/books/whose-summit-whose-information-society

[7] Task Force on Financial Mechanisms. (2004). The Report of the Task Force on Financial Mechanisms for ICT for Development. https://www.itu.int/net/wsis/tffm/final-report.pdf

[8]Navas-Sabater, J., Dymond, A., & Juntunen, N. (2002). Telecommunications and Information Services for the Poor: Toward a Strategy for Universal Access. World Bank. https://doi.org/10.1596/0-8213-5121-4

[10] ITU. (2020). Connecting humanity: Assessing investment needs of connecting humanity to the Internet by 2030. https://www.itu.int/dms_pub/itu-d/opb/gen/D-GEN-INVEST.CON-2020-PDF-E.pdf

[11] Digital Development Partnership. (2022). DDP Annual Review 2022: Towards green, resilient and inclusive digitalization. World Bank. https://indd.adobe.com/view/6a1d7a70-3b72-498d-afba-64fb0f84a8e6

[15] Zibi, G. (2018). Closing the Investment Gap: How Multilateral Development Banks Can Contribute to Digital Inclusion. World Wide Web Foundation & Alliance for Affordable Internet. https://a4ai.org/wp-content/uploads/2018/04/MDB-Investments-in-the-ICT-Sector.pdf

[16] World Bank Development Committee. (2023). Ending Poverty on a Livable Planet: Report to Governors on World Bank Evolution. https://www.devcommittee.org/content/dam/sites/devcommittee/doc/documents/2023/Final%20Updated%20Evolution%20Paper%20DC2023-0003.pdf

[17] https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/stronger-europe-world/global-gateway_en

[18] Keith, T. (2022, 26 June). Biden announced a $600 billion global infrastructure program to counter China's clout. NPR. https://www.npr.org/2022/06/26/1107701371/biden-announced-a-600-billion-global-infrastructure-program-to-counter-chinas-cl

[20] United Nations Conference on Trade and Development. (2023). World Investment Report 2023: Investing in sustainable energy for all. https://unctad.org/system/files/official-document/wir2023_en.pdf

[22] Inter-agency Task Force on Financing for Development. (2022). Financing for Sustainable Development Report 2022. United Nations. https://www.un.org/ohrlls/sites/www.un.org.ohrlls/files/fsdr_2022.pdf

[23] Thakur, D., & Potter, L. (2018). Universal Service and Access Funds: An Untapped Resource to Close the Gender Digital Divide. Web Foundation. http://webfoundation.org/docs/2018/03/Using-USAFs-to-Close-the-Gender-Digital-Divide-in-Africa.pdf

[24] Working Group for the Broadband Commission for Sustainable Development. (2021). 21st Century Financing Models for Bridging Broadband Connectivity Gaps. https://broadbandcommission.org/publication/21st-century-financing-models

[27] Shanahan, M., & Bahia, K. (2023). Op. cit.

[28] ITU. (2022, 19 April). New UN targets chart path to universal meaningful connectivity. https://www.itu.int/hub/2022/04/new-un-targets-chart-path-to-universal-meaningful-connectivity

[29] ITU. (2020). Op. cit.

[30] Rey-Moreno, C., et al. (2021). Funding Bottom-up Connectivity: Approaches and Challenges of Community Networks to Sustain Themselves. In L. Belli & S. Hadzic (Eds.), Community Networks: Towards Sustainable Funding Models. FGV Direito Rio. https://comconnectivity.org/wp-content/uploads/2021/12/Community-Networks-Towards-Sustainable-Funding-Models.pdf

[31] Bidwell, N. J., & Jensen, M. (2019). Bottom-up connectivity strategies: Community-led small-scale telecommunication infrastructure networks in the global South. APC. https://www.apc.org/sites/default/files/bottom-up-connectivity-strategies_0.pdf

[32] Forster, J., Matranga, B., & Nagendra, A. (2022). Financing mechanisms for locally owned internet infrastructure. APC, Connect Humanity, Connectivity Capital & the Internet Society. https://www.apc.org/en/pubs/financing-mechanisms-locally-owned-internet-infrastructure

[33] Bidwell, N. J., & Jensen, M. (2019). Op. cit.

[34] As mentioned above, the funding may help traditional players cover the startup costs, but it will not help them sustain and maintain these networks in the long run, given the low ARPU in these areas.

[35] APC, Redes A.C., & Universidad Politécnica de Catalunya. (2020). Expanding the telecommunications operators ecosystem: Policy and regulatory guidelines to enable local operators. APC. https://www.apc.org/en/pubs/expanding-telecommunications-operators-ecosystem-policy-and-regulatory-guidelines-enable-local

[37] ITU. (2022). World Telecommunication Development Conference 2022 (WTDC-22): Final Report. https://www.itu.int/dms_pub/itu-d/opb/tdc/D-TDC-WTDC-2022-PDF-E.pdf

[38] Giga & Boston Consulting Group. (2021). Meaningful school connectivity: An assessment of sustainable business models. ITU. https://giga.global/bcg-report

[39] Postal and Telecommunications Regulatory Authority of Zimbabwe Licence Fee Categories. http://www.potraz.gov.zw/wp-content/uploads/2022/03/Licence-Categories-Including-Fees.pdf

[40] Uganda Communications Commission Communal Access Provider License. https://www.ucc.co.ug/wp-content/uploads/2023/10/DESCRIPTION-OF-TELECOM-LICENSES-AND-AUTHORISATIONS.pdf

[41] Ethiopian Communication Authority’s Telecommunications Licensing Directive 792-2021. https://chilot.blog/wp-content/uploads/2023/02/daf6f-telecommunications-licensing-directive.pdf

[42] Communications Authority of Kenya Community Networks Service Provider Licence. https://www.ca.go.ke/sites/default/files/articles/Telecoms%20Forms/Application%20Form%20For%20Community%20Network%20and%20Service%20Provider%20Licence1-TL-8-0.pdf

[43] South African Government Electronic Communications Amendment Bill: Draft. https://www.gov.za/documents/electronic-communications-amendment-bill-draft-23-jun-2023-0000

[44] Competition Commission of South Africa. (2019). Data Services Market Inquiry: Final Report. https://www.compcom.co.za/wp-content/uploads/2019/12/DSMI-Non-Confidential-Report-002.pdf

[45] Contreras García, V. (2023, 4 July). Gustavo Petro firma decreto para que comunidades autogestionen su Internet fijo. DPL News. https://dplnews.com/gustavo-petro-firma-decreto-para-que-comunidades-autogestionen-su-internet-fijo/

[46] Agência Nacional de Telecomunicações. (2023, 4 December). Publicado relatório com atividades realizadas pelo Grupo de Trabalho sobre Redes Comunitárias. https://www.gov.br/anatel/pt-br/assuntos/noticias/publicado-relatorio-com-atividades-realizadas-pelo-grupo-de-trabalho-sobre-redes-comunitarias

[47] ITU Global Symposium for Regulators. (2021). Best Practice Guidelines. https://www.itu.int/en/ITU-D/Conferences/GSR/2021/Documents/GSR-21_Best-Practice-Guidelines_FINAL_E_V2.pdf

[48] Broadband Commission Working Group on Broadband for All. (2019). A “Digital Infrastructure Moonshot” for Africa. https://www.broadbandcommission.org/Documents/working-groups/DigitalMoonshotforAfrica_Report.pdf and Working Group for the Broadband Commission for Sustainable Development. (2021). Op. cit.

[51] https://ca.go.ke/sites/default/files/CA/Strategic%20Plan/CA%20Strategic%20Plan%202023-2027%20Final.pdf

[52] There are plans to support 30 community networks during the period covered. See: Mlanjira, D. (2022, 20 May). MACRA launches Universal Service Fund's strategic plan. Nyasa Times. https://www.nyasatimes.com/macra-launches-universal-service-funds-strategic-plan/

[53]https://uas.nicta.gov.pg/index.php/consultations/10-uas-projects-consultations/70-public-consultation-uas-strategic-plan-2023-2027-and-proposed-uas-projects-for-2023

[55] Working Group for the Broadband Commission for Sustainable Development. (2021). Op. cit.

[56] García Zeballos, A., et al. (2021). Development of National Broadband Plans in Latin America and the Caribbean. Inter-American Development Bank. https://publications.iadb.org/en/development-national-broadband-plans-latin-america-and-caribbean

[57] Brewer, J., Jeong, Y., & Husar, A. (2022). Last Mile Connectivity: Addressing the Affordability Frontier. Asian Development Bank. https://www.adb.org/publications/last-mile-connectivity-affordability-frontier

[58] Degezelle, W. (2022). The Open Internet as cornerstone of digitalization. European Commission. https://fpi.ec.europa.eu/news-1/new-report-released-open-internet-opportunities-eu-africa-partnership-2022-10-24_en

[59] Even though the absolute number of people connected is slowly increasing, the impact of COVID-19 in driving services, employment and social interactions online has increased our overall societal dependence on digital infrastructure. This means that all those without affordable access are at an increasing disadvantage. Rising demand for broadband also means that those with only weak or unaffordable connectivity who might otherwise have been considered connected are still without meaningful access.

[60] Brito, C. (2020, 24 September). COVID-19 has intensified the digital divide. World Economic Forum. https://www.weforum.org/agenda/2020/09/covid-19-has-intensified-the-digital-divide

[61] Forster, J., Matranga, B., & Nagendra, A. (2022). Op. cit.

[63] Martens, J. (2023). Reforms to the global financial architecture. Global Policy Forum. https://www.globalpolicy.org/sites/default/files/download/Briefing_Reforms%20to%20the%20global%20financial%20architecture.pdf

[65] Gilbert, L. (2022, 18 July). Open Philanthropy Shallow Investigation: Telecommunications in LMICs. Effective Altruism Forum. https://forum.effectivealtruism.org/posts/H6GhXkbfAy949xhGf/open-philanthropy-shallow-investigation-telecommunications

[66] Connect Humanity. (2022). Funding to bridge the digital divide: U.S. philanthropic giving to digital equity causes. https://connecthumanity.fund/research-philanthropic-giving-to-digital-equity

[67] USAID. (2023, 7 April). Women in the Digital Economy Fund. https://www.usaid.gov/digital-development/gender-digital

[68] https://www.apc.org/en/grants-local-implementation-apcs-strategic-plan-2022#Altermundi

Notes:

This report was originally published as part of a larger compilation: “Global Information Society Watch 2024 Special edition: WSIS+20: Reimagining horizons of dignity, equity and justice for our digital future"

Creative Commons Attribution 4.0 International (CC BY 4.0) - Some rights reserved.

Web and e-book

ISBN: 978-92-95113-67-1

APC-202404-APC-R-EN-DIGITAL-357

Print

ISBN:978-92-95113-68-8

APC-202404-APC-R-EN-P-358